0.31%

0.31%

In May Bloomberg Aggregate Bond Index

0.49%

0.49%

In May Bloomberg U.S Corporate High Yield Index

Geopolitical and Economic Update:

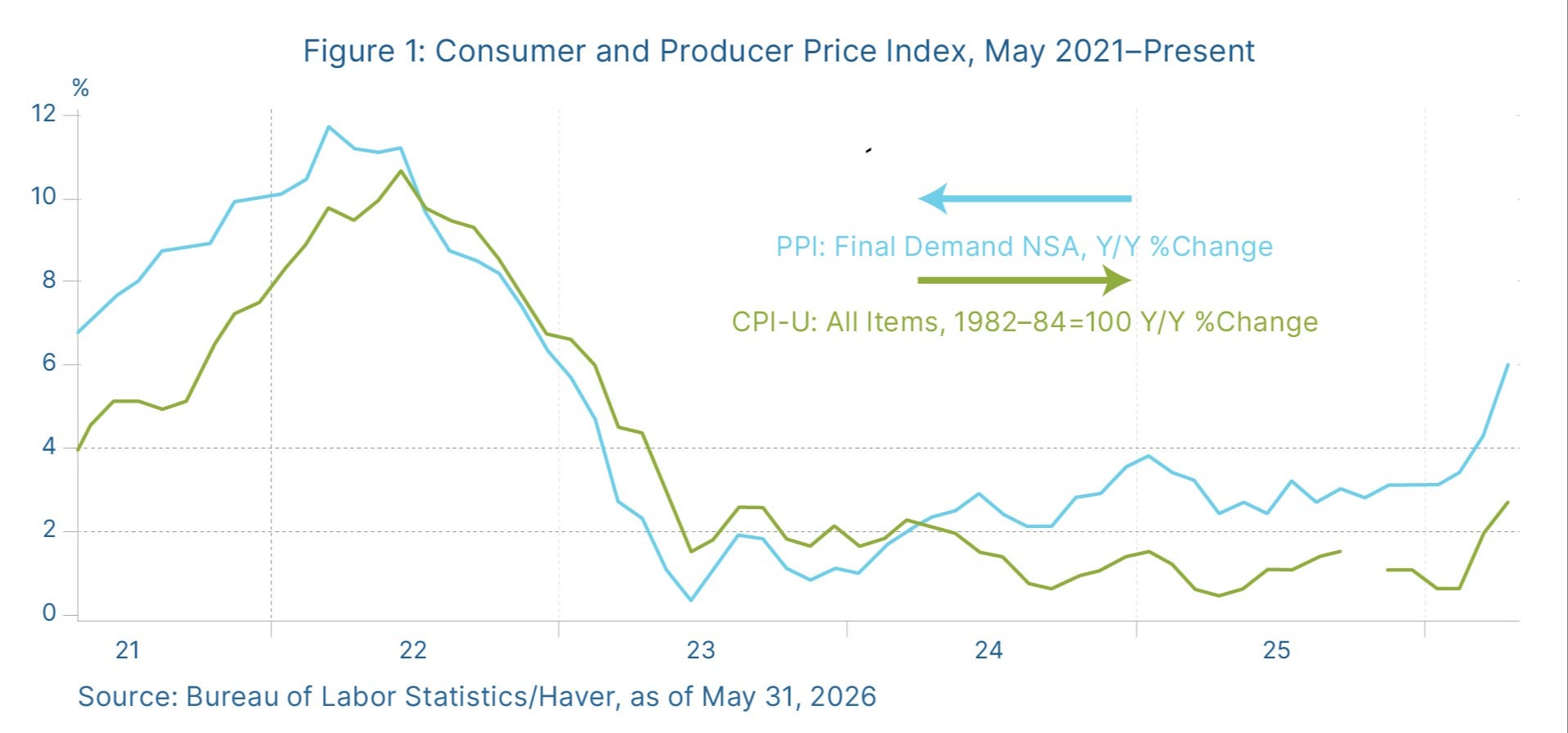

Mixed Economic Data and Headline Risks

The economic updates released last month were mixed but continued to indicate a growing economy. Not surprisingly given the recent surge in oil prices, both the Consumer Price Index (CPI) and the Producer Price Index (PPI) came in higher than anticipated for April. Consumer prices rose at an annual rate of 3.81 percent. Even more concerning was the increase in producer prices, which rose 6 percent. While we are still a long way from inflation reaching the levels seen in 2022, when the Fed reacted by raising interest rates aggressively, this needs to be watched going forward. Without a settlement in the Middle East that fully reopens the Strait of Hormuz and returns oil supply to prewar level, sticky inflation will continue to be an issue for markets.

On the positive front, the April employment report again came in above expectations, with 115,000 jobs created. This followed March’s strong 185,000 jobs created. Personal spending also rose for the month following strong spending data in the previous month. Put together, this indicates that consumers are still in a solid place despite the rise in oil prices.

Solid job growth and a consumer that continues to spend should buy the Federal Reserve time to wait to see the path for inflation before needing to adjust interest rate policy. This also allows new Fed chair Kevin Warsh time to transition to his new role without needing to immediately react to any deteriorating data.